In the 1680s there was a coffee house in London by the name of "Lloyd's". This place, catering to early maritime insurers, lent its name to the nascent English insurance market place, the now famous Lloyd's of London.

Less than a decade later, the English insurance market was thrown into crisis. A fleet of French privateers attacked an Anglo-Dutch merchant fleet in the battle of Lagos in 1693, causing estimated losses of around 1 million British pounds, more than a percent of the English GDP at the time. 33 insurers went bankrupt, a significant part of the industry.

The nascent sector had failed to diversify their risks sufficiently. The probability of risk events like this one is hard to predict; it follows a heavy-tailed distribution. This is still the case today. We also still have unexpected risk events - take the Covid-19 pandemic. Of course, the industry is more mature today, the sector more diverse. But there are still bottlenecks, where everyone may bet on the same card, and where the chance to diversify is limited. There are, for instance, only three important providers of professional risk models, RMS, EQECAT, and AIR - and in many cases only one risk model is used. Risk models are important for catastrophe insurance, i.e. insurance against catastrophe events, hurricanes, flooding, earthquakes, etc., where the distribution and expectation of damages is dominated by large but rare events (heavy-tailed damage distributions). Every risk model is inaccurate, so everyone is wrong occasionally - but it is really bad if everyone is wrong at the same time, giving rise to a kind of systemic risk unique to insurance.

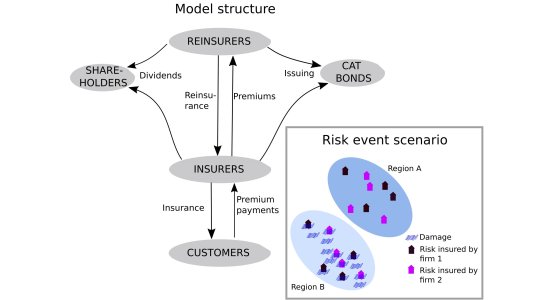

In our paper, published in the Journal of Economic Interaction and Coordination, we, Oxford Mathematicians Torsten Heinrich and Doyne Farmer and Oxford Researcher and former Oxford Mathematics Postdoc Juan Sabuco, assess this type of systemic risk from model homogeneity. We propose an agent-based model for this purpose. Agent-based models (ABM) represent heterogeneous agents and their interactions directly and can be simulated to study the behavior of such systems while retaining much of the original systems' complexity. This makes them well-suited to study catastrophe insurance with its heavy-tailed damage distributions. The figure shows the structure of the ABM, its agents, and illustrates the type of catastrophic risks insured by the sector the model represents.

We use our ABM to run 400 simulations each in four different scenarios, first with firms using one risk model (the lowest level of risk model diversity), then with firms using two, three, and four risk models respectively. We designed our risk models to be imperfect; in other words, true to real life, they inevitably fail to accurately predict catastrophes. Our four risk-models are intentionally imperfect, but in different ways. They underestimate and overestimate different types of perils and thus fail to accurately predict the risks faced by different geographical locations.

Our results confirmed worries that the industry currently uses dangerously few risk models. Moreover, we were able to quantify the impact of this: compared to risk model homogeneity (one risk model), settings with four risk models, for instance, allow around 20% more insurance firms to survive in the industry (on average), the number of non-insured risks to be halved, and available capital to be increased by 50%. Our ABM can also be used to investigate other phenomena in catastrophe insurance.

Recent events in connection with the Covid-19 pandemic highlight why systemic risk in catastrophe insurance is an important issue: its impacts on catastrophe insurance are varied, ranging from business interruption and delays in logistics (shipping etc.) to claims resulting from Covid-19 deaths or from hospitals' professional liability to bankruptcies in the tourism and hospitality sector. However, we have not experienced pandemics of this scale in modern times. Not only could risks resulting for catastrophe insurance not have been foreseen, there are no previous data with which these risks could have been estimated. Inaccurate risk predictions are unavoidable, losses are unavoidable, but diversity in modeling may prevent a bankruptcy cascade and the collapse of the insurance system in such cases.