Multisensor data fusion in the frame of the TBM on reals. Application to land vehicle positioning

Caron, F

Smets, P

Duflos, E

Vanheeghe, P

volume 2

1473-1480

(01 Jan 2005)

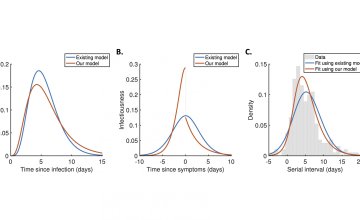

Oxford Mathematician William Hart and former Oxford Mathematician Dr Robin Thompson (now an Assistant Professor at the University of Warwick) discuss their latest joint COVID-19 research (carried out with fellow Oxford Mathematician Philip Maini), using mathematical models to infer changes in infectiousness during SARS-CoV-2 infections.

Fri, 18 Jun 2021

13:30 -

17:00

Groups and Geometry in the South East

Piotr Przytycki, Elia Fioravanti, Rylee Lyman

(McGill & Bonn & Rutgers-Newark)

Further Information

Tits Alternative in dimension 2

1:30-2:30PM

Piotr Przytycki (McGill)

A group G satisfies the Tits alternative if each of its finitely generated subgroups contains a non-abelian free group or is virtually solvable. I will sketch a proof of a theorem saying that if G acts geometrically on a simply connected nonpositively curved complex built of equilateral triangles, then it satisfies the Tits alternative. This is joint work with Damian Osajda.

Coarse-median preserving automorphisms

2:45-3:45PM

Elia Fioravanti (Bonn)

We study fixed subgroups of automorphisms of right-angled Artin and Coxeter groups. If Phi is an untwisted automorphism of a RAAG, or an arbitrary automorphism of a RACG, we prove that Fix(Phi) is finitely generated and undistorted. Up to replacing Phi with a power, the fixed subgroup is actually quasi-convex with respect to the standard word metric (which implies that it is separable and a virtual retract, by work of Haglund and Wise). Our techniques also apply to automorphisms of hyperbolic groups and to certain automorphisms of hierarchically hyperbolic groups. Based on arXiv:2101.04415.

Some new CAT(0) free-by-cyclic groups

4:00-5:00PM

Rylee Lyman (Rutgers-Newark)

I will construct several infinite families of polynomially-growing automorphisms of free groups whose mapping tori are CAT(0) free-by-cyclic groups. Such mapping tori are thick, and thus not relatively hyperbolic. These are the first families comprising infinitely many examples for each rank of the nonabelian free group; they contrast strongly with Gersten's example of a thick free-by-cyclic group which cannot be a subgroup of a CAT(0) group.

Symbolic Reachability Analysis of High Dimensional Max-Plus Linear Systems

Mufid, M

Adzkiya, D

Abate, A

IFAC-PapersOnLine

volume 53

issue 4

459-465

(2020)

Tue, 22 Jun 2021

11:00

11:00

Virtual

90 minutes of CCC

Roger Penrose et al.

Abstract

This is a joint GR-QFT seminar, to celebrate in advance the 90th birthday of Roger Penrose later in the summer, comprising 9 talks on conformal cyclic cosmology. The provisional schedule is as follows:

11:00 Roger Penrose (Oxford, UK) : The Initial Driving Forces Behind CCC

11:10 Paul Tod (Oxford, UK) : Questions for CCC

11:20 Vahe Gurzadyan (Yerevan, Armenia): CCC predictions and CMB

11:30 Krzysztof Meissner (Warsaw, Poland): Perfect fluids in CCC

11:40 Daniel An (SUNY, USA) : Finding information in the Cosmic Microwave Background data

11:50 Jörg Frauendiener (Otago, New Zealand) : Impulsive waves in de Sitter space and their impact on the present aeon

12:00 Pawel Nurowski (Warsaw, Poland and Guangdong Technion, China): Poincare-Einstein expansion and CCC

12:10 Luis Campusano (FCFM, Chile) : (Very) Large Quasar Groups

12:20 Roger Penrose (Oxford, UK) : What has CCC achieved; where can it go from here?

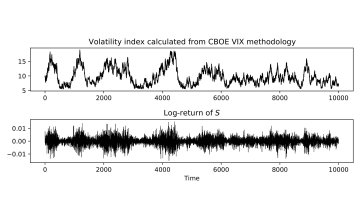

Oxford Mathematicians Samuel N. Cohen, Christoph Reisinger and Sheng Wang have developed new methods to help machine learning build economically reasonable models for options markets. By embedding no-arbitrage restrictions within a neural network, more trustworthy and realistic models can be built, allowing for better risk management in the banking system.

Thu, 17 Jun 2021

10:00

10:00

Virtual

Systolic Complexes and Group Presentations

Mireille Soergel

(Université de Bourgogne)

Abstract

We introduce the notion of systolic complexes and give conditions on presentations to construct such complexes using Cayley graphs.

We consider Garside groups to find examples of groups admitting such a presentation.