The final Fridays@11 session of the year is here, and it's going to be a really useful session on preparing for Prelims exams!

The final Fridays@11 session of the year is here, and it's going to be a really useful session on preparing for Prelims exams!

It's the Week 2 Student Bulletin!

It's the Week 2 Student Bulletin! To celebrate International Women in Mathematics Day (May 12), Mathematrix is hosting a pizza lunch where we will watch ‘Journeys of Women in Mathematics’, a powerful 20-minute film by the International Mathematical Union showcasing the experiences of women mathematicians worldwide.

The film follows three mathematicians from India, Cameroon, and Brazil from their home institutions to the (WM)² international meeting, showing their research and what it’s like to be part of the global maths community.

The Anti-Racism Ally Network runs a range of events across the term as well as having a

The Knowledge Exchange Hub for the Mathematical Sciences has commissioned the award winning Active Bystander Training Company to deliver a focused, practical session designed to empower our community to challenge unacceptable behaviours — including those that may have become normalised over time.

Wednesday 20 May, 10:00 am - 11:30 am. Online and free

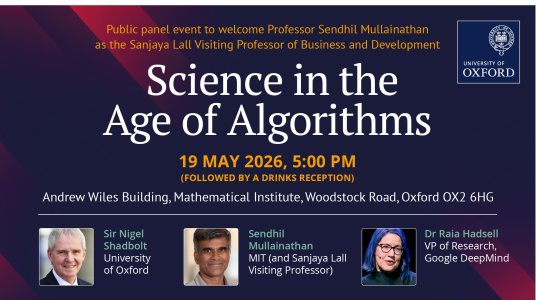

Science in the Age of Algorithms: Rethinking Discovery in the AI Era

Participants:

- Sendhil Mullainathan, Peter de Florez Professor of Economics & Computer Science, MIT (and Sanjaya Lall Visiting Professor, Oxford)

- Sir Nigel Shadbolt, Principal of Jesus College and Professor of Computer Science, Oxford

- Dr Raia Hadsell, VP of Research, Google DeepMind

- Chair: Professor Johannes Abeler, Professor & Head of Economics Department, Oxford

5 pm, 19 May, Andrew Wiles Building